New Frontier is a research and registered investment advisory firm with over a decade of experience as an ETF asset manager.

Efficient Frontiers in Theory and Practice: Longer Horizons Deliver Better Wealth Security

Most students of modern finance are familiar with the efficient frontier chart, which shows the range of expected returns and risks for optimized portfolios. Because these calculations are performed when the portfolios are constructed, before they are invested, the values on the chart are estimates, almost sure to differ from the observed risks and returns.

An Important Difference between Michaud and Classical Frontiers

One of the benefits of the Michaud optimization procedure is that real performance is likely to be closer to estimated performance than the corresponding classical mean-variance optimization. This is because the Michaud process considers estimation error, and investments end up allocating more evenly among similar assets rather than going all in on the slightly better asset (on paper). The resulting better diversified portfolio tracks expectations more closely over time. Of course, risky investments are often dominated by volatile market trends, so over shorter time horizons, realized returns can always differ from expectations. However, up and down market cycles tend to balance each other out over time, so longer-term investments generally hew more closely to their expectations.

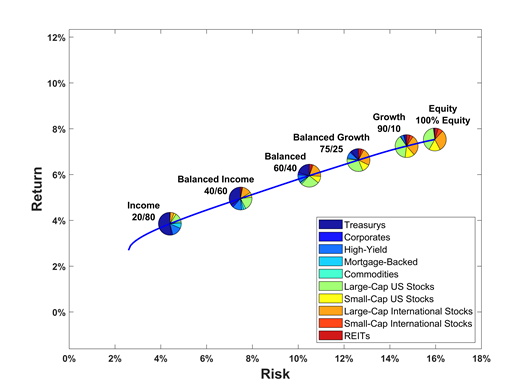

New Frontier offers portfolios at different risk levels on the efficient frontier. Figure 1 shows an efficient frontier calculation for our Global Core ETF Portfolios. Six risk profiles on the frontier represent a range of investor preferences from conservative (risk-averse) to aggressive (seeking greater returns). In the graph, the Return on the y-axis gives a rough estimate for the center of the range of returns, and the Risk (standard deviation) on the x-axis measures how variable around this center the returns might be. This means that the aggressive profiles are expected to perform better on average, but during a short period might do better or worse than the more conservative profiles.

Figure 1: An Efficient Frontier for New Frontier Global Core ETF Portfolios

Source: New Frontier Advisors, as of April 2023. The pie charts show different compositions ranging from conservative (80% bonds) to aggressive (100% equities).

Realized Performance of New Frontier’s Portfolios

The idea of an efficient frontier could be extended to graph realized performance of investments. Similarly to the theoretical efficient frontier, the realized returns would be on the y-axis and the standard deviations would be on the x-axis. In contrast to the theoretical frontier, the values on the graph are precisely the realized performance and no longer represent a range of unknown values. The interpretation of the return is straightforward, and the standard deviation corresponds to how variable the monthly returns were during the time period of the graph.

Next we will present some realized frontiers for New Frontier’s Global Standard Strategy. Given the inception in 2004, there are many windows of monthly historical performance over one- and even ten- year spans, considering them all should give a good idea of historical performance ranges for these time horizons. While the one-year returns range from very poor to very excellent, with wider ranges for the riskier profiles, the ten-year returns show more reliability. All the figures below are calculated from the New Frontier Indices, which quite precisely track performance of the corresponding New Frontier ETFs.

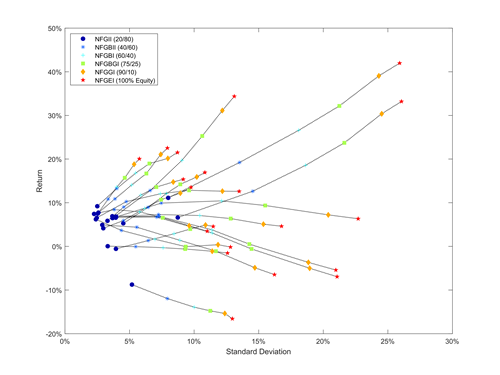

Figure 2 shows 20 randomly selected one-year histories. As might be expected, these vary widely in performance. Usually, the order from conservative to aggressive is preserved in the return rankings, but in years when bonds and stocks perform differently, the ranks may be out of order.

Figure 2: Randomly Selected One-year Histories of the Six New Frontier Global Standard Indices

Source: New Frontier Advisors, as of April 2023.

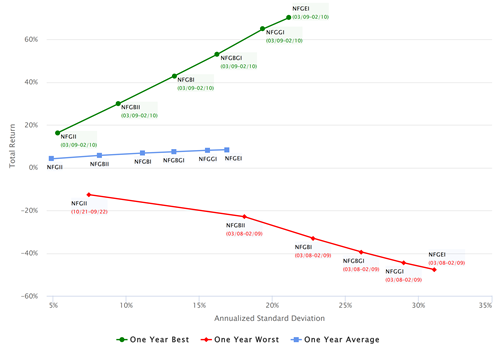

Figure 3 displays the best- and worst-case scenarios for the one-year returns. In any one year, markets can perform poorly, and in some years, all asset classes perform poorly. On the other hand, some years have great returns for all asset classes. The expectation is that the good years balance the bad years over time and lead to positive investment outcomes. The averages over all time windows for all six risk profiles are shown in this chart, and they are close to the original efficient frontier estimates in Figure 1.

Figure 3: Best- and Worst-Case Scenarios for One-year Windows from Historical Performance of the Six Risk profiles of New Frontier’s Global Standard Indices

Source: New Frontier Advisors, as of April 2023.

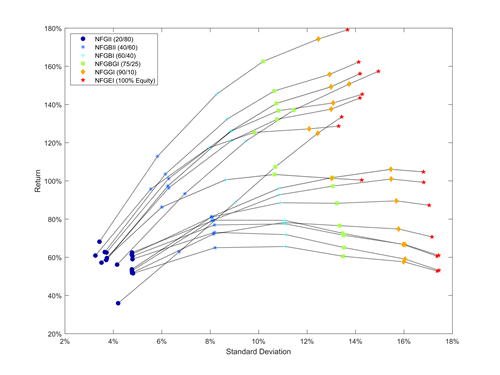

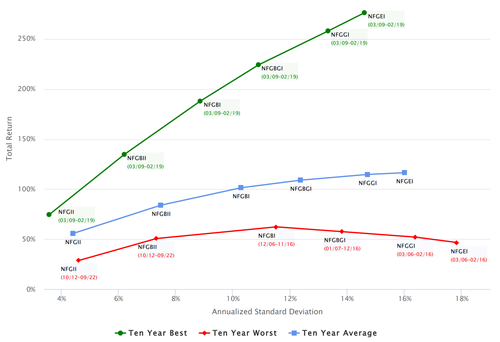

Figures 4 and 5 illustrate ten years of performance data and correspond to Figures 2 and 3. These charts tell a very different story when it comes to long-term positive returns. The randomly selected ten-year intervals tend to align more closely, and the best-case scenario in Figure 5 exhibits outstanding performance, whereas the worst-case scenario this time is positive for all six profiles. In the worst case, the balanced profile (60/40), provides more protection from loss, leading to better performance in this worst case. This may be explained by better diversification in the balanced profile across asset classes.

Figure 4: Randomly Selected 10-year Historical Performance of the Six New Frontier Global Standard Indices

Source: New Frontier Advisors, as of April 2023.

Figure 5: Best- and Worst-Case Scenarios for 10-year Periods from Historical Performance of the Six Risk Profiles of New Frontier’s Global Standard Indices

Source: New Frontier Advisors, as of April 2023.

Long-term Performance Advantages

These charts demonstrate the long-term advantages of effective diversification, optimization, and risk control in New Frontier’s multi-patented investment process. Since markets are unpredictable and some years perform better than others, any one year can have performance that is better or worse than expected. Given that performance ranges increase for riskier profiles, the worst become worse, and the best become better.

The good news is that for all six profiles, over periods of at least ten years, the worst possible performance over the entire history which includes two major crash years, is a positive return around +50%. The best-case performance increases with risk on the frontier, and the best risk protection is seen in the balanced 60/40 strategy (NFGBI).

Although historical performance is no guarantee of future performance, the data shows a long history of positive long-term performance. Importantly, the realized performance of our globally diversified strategies effectively demonstrates the robustness of our optimization approach over many different market cycles.

DISCLOSURES

This information is for information purposes only. It does not constitute an offer or solicitation of securities or investment services or an endorsement thereof in any jurisdiction or in any circumstance in which such offer or solicitation is unlawful or not authorized. None of the information contained in this report constitutes, or is intended to constitute, a recommendation of any particular security or trading strategy or a determination by New Frontier that any security or trading strategy is suitable for any specific person. To the extent any of the information contained herein may be deemed to be investment advice, such information is impersonal and is not tailored to the investment needs of any specific person. All investments carry a risk of loss, including the possible loss of principal. There is no assurance that any investment will be profitable.

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.

To receive additional information such as the New Frontier brochure (the ADV Part 2), please contact Nicholas Lam at nlam@newfrontieradvisors.com.

comments powered by Disqus

Locate Us

New Frontier Advisors

155 Federal Street

Boston, MA 02110

617.482.1433

Contact us to find out how you can invest in New Frontier portfolios.