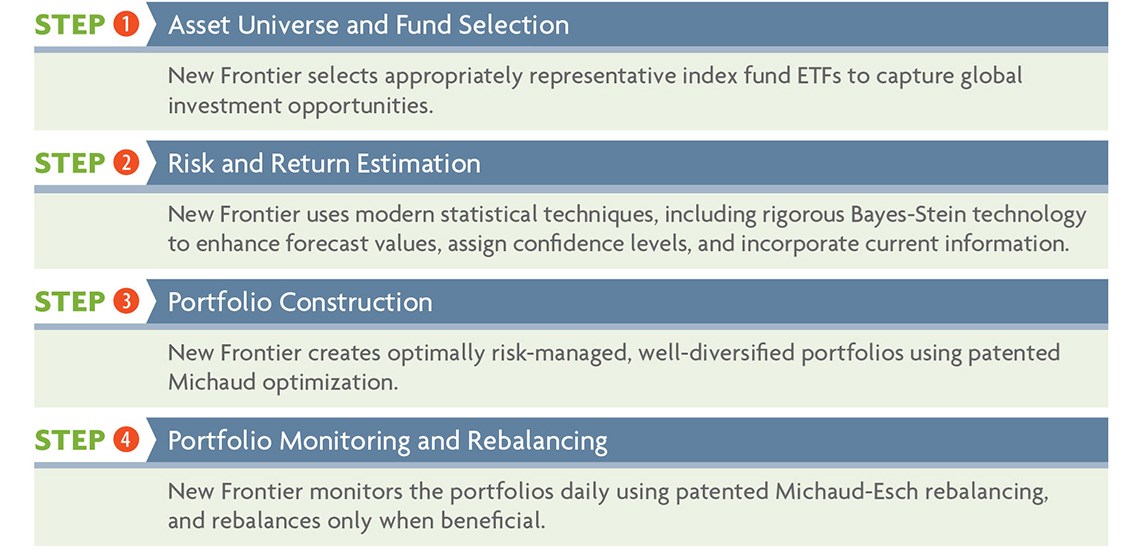

Our Process

New Frontier adds value to all four stages of our investment process with institutional expertise and patented technologies. The four steps of our investment process are: Asset Universe and Fund Selection, Risk and Return Estimation, Portfolio Construction, and Portfolio Monitoring and Rebalancing.

Step 1: Asset Universe and Fund Selection

New Frontier chooses 15-30 ETFs that span worldwide sources of investable economic growth to obtain a meaningful representation of the world’s fundamental factors. Our global scope allows us to consider the most attractive investment opportunities wherever they may lie for return enhancement as well as risk reduction through diversification. We have used ETFs since they first became available because of their transparency, tax efficiency, and liquidity. As an independent institutional manager, New Frontier is able to select the most liquid and representative ETFs, independent of fund family.

Step 2: Risk and Return Estimation

New Frontier uses state-of-the-art statistical techniques to improve the risk and return estimates derived from capital market and fund data. Our investment committee incorporates current information, including regulatory, economic, financial, and other factors affecting global capital markets, with advanced statistical methods.

New Frontier uses modern statistics to enhance the forecast value of historically estimated information and to integrate contemporary market data such as the yield curve, as well as global economic and regulatory developments, into the estimation process. New Frontier's estimates optimally reflect investment theory and display sensitivity to current market conditions without directional forecasts.

Step 3: Portfolio Construction

New Frontier is globally recognized for its innovations in portfolio management which uniquely and properly address uncertainty in investment information. Commercially available optimizers typically treat investment information as if it is certain, even though investment information is inherently uncertain. This is why traditionally optimized portfolios are known to have poor performance characteristics.

New Frontier accounts for this uncertainty in its investment process. All of our portfolios are constructed with Michaud optimization. Michaud optimization explores the many ways that assets may perform in the future by way of advanced statistics. It treats investment information realistically. The resulting efficient frontier is more stable and produces more diversified, investment intuitive, and effective optimal portfolios. In independent tests, the Michaud portfolios performed better than traditionally optimized portfolios. Michaud optimization sets the world standard for effective portfolio construction.

New Frontier’s asset allocation process features Michaud optimization for all of our portfolios. Each portfolio is constructed to be optimal for the specific investment objective. For instance, tax-sensitive portfolios are optimized with tax-sensitive Michaud optimization. As a result, all of New Frontier’s portfolios feature effective diversification, managed risk, and enhanced performance.

Step 4: Portfolio Monitoring and Rebalancing

New Frontier’s resampling technology represents the first truly effective portfolio monitoring and rebalancing procedure. Traditional monitoring and rebalancing practices are typically ad hoc and often lead to trading in statistical noise or not trading when information may be available. As a consequence, trades can be ineffective and costly.

New Frontier's portfolio monitoring and trading decisions are based on Michaud-Esch rebalancing technology. The multi-patented technology provides the first rigorous statistical test for the decision to trade. It enhances investment value by recommending trading only when likely to be effective. New Frontier applies this test separately for each strategy it manages. The methodology uses Monte Carlo simulation to evaluate the likelihood that the current portfolio and the optimal portfolio will perform in a similar manner in the investment period. The procedure finds the probability that trading is required to maintain a diversified risk-controlled optimal portfolio. This unique technology is designed to avoid trading in noise and to recommend trading when the available information warrants it.