Note to Investors - Volatility: Russia and Ukraine

Many have been concerned about recent heightened volatility in US markets. Indeed, the CBOE Volatility Index (VIX) attained a high of 38.94 on Monday, January 24, 2022, a level not seen since October of 2020, and US indices had extreme intra-day movement on several days during the same week. Some of this volatility may be driven by anticipation of rising interest rates, but interest rate policy changes do not fully explain such extreme price movement in US equity markets. Our position on interest rate changes has been clarified in recent blog posts.

The remaining uncertainty in US capital markets is likely being driven by geopolitical risk, notably the imminent threat of a Russian invasion in Ukraine. Were this threatened invasion to happen, it would not be the first time in recent history that Russia has invaded Ukraine. In 2014 Russia massed military forces, annexed Crimea, and fomented violent unrest throughout Ukraine. This history may be relevant to today's situation, and it's worth taking another look at that invasion to examine how it affected global investors.

It’s worth noting that none of New Frontier’s funds have any direct exposure to Ukrainian securities, but there is some small exposure to Russian equities in an Emerging Markets ETF, making up a few basis points of the total equity exposure in our global ETF portfolios.

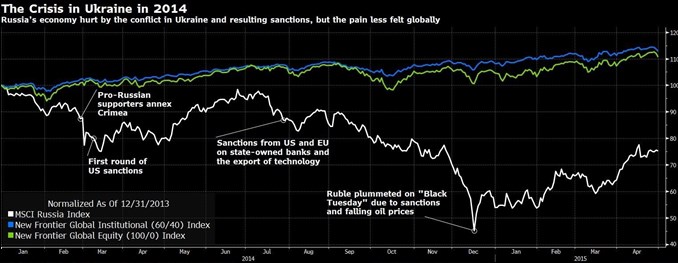

The figure below shows New Frontier’s NFGBI (60/40) and NFGEI (All-Equity) indices and the MSCI Russia index during the time period of the 2014-2015 invasion of Crimea and Ukraine. The direct impact of the invasion is insignificant for the New Frontier funds, but the Russian index shows a steep decline over the period. Interestingly the Russian Index continues to decline in waves through the entire year and even into the following year as the crisis continues and reaches its final stages.

Source: Bloomberg. A timeline of the last Russia-Ukraine crisis, showing the performance of New Frontier's Global Institutional and All-Equity indices, and the MSCI Russia Index. The Russian index bore the brunt of the conflict and the global funds were relatively unaffected.

Once again, Russia’s actions have impacted its own market far more than the rest of the world’s. Year-to-date in 2022, Russia is by far the worst performing asset in Emerging Markets with a return of -16.17% as of January 26. To frame that underperformance, the second worst country in the Emerging markets over the same period was Mexico, with a -4.97% return.

Russia’s weight of less than 3% weight in emerging markets indices ensures even severe underperformance of its stock market will have no significant impact on the performance of New Frontier portfolios. Should the current conflict play out similarly to 2014-15, it would be unlikely to have any substantial impact for New Frontier investors. However, this time could be different—fear of supply disruptions has already rattled the tight commodity markets and sent energy prices higher. More significantly, we know the previous crisis never spread into a broad multi-national war and clearly a serious military conflict could have a devastating impact on the global economy and markets.

In conclusion, the previous Russian invasion of Ukraine had negligible consequences for New Frontier as well as most US investors. While we are vigilantly watching the situation in this part of the world, theoretical and empirical evidence shows optimized and globally diversified multi-asset portfolios cushion investors from many geopolitical crises. Particularly in times of future uncertainty, the most important consideration is ensuring your portfolio has the right investment objective and risk tolerance for you.

Disclosures: New Frontier Advisors LLC (“New Frontier”) is a federally registered investment adviser based in Boston, MA. The information discussed here is for information purposes only. Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.

comments powered by Disqus

Locate Us

New Frontier Advisors

155 Federal Street

Boston, MA 02110

617.482.1433

Contact us to find out how you can invest in New Frontier portfolios.