Global Yields: Framing Today’s Low Yield in a Global and Historical Context

The Fed potentially winding down fiscal stimulus raises the question of whether current interest rates are sustainable. But investors have been concerned whether interest rates were too low for more than a decade. Seven years ago, in response to continued concern over the viability of investing in bonds, I made a case that rates in the US did not have to go up given the existing far lower international rates in our 2014 blog. The overwhelming sentiment was that interest rates “must go up.” The educated consensus was that the low rates in the US were economically unsustainable for more than the very short term and the 10-year rate would necessarily revert to the “normal” range of 4-5%. Since investors were focused on US Treasury rates, I thought it would be instructive to examine US rates in a global context.

In the global context, US rates looked comparatively high. Then (as now) rates in developed and even many emerging economies were much lower than in the US. To get a higher yield, one had to lend to small economies with concerns of default. The global context suggested both that rates could go lower, and that US Treasurys had an acceptable yield for their risk. This perspective reinforced our conviction in the value of US Treasurys in a portfolio optimized for an unknown future—a consistent approach which has rewarded our investors over time.

What does the global picture look like today?

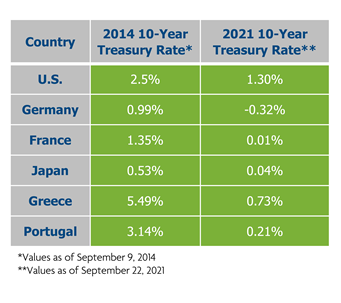

Clearly the past consensus on the direction of interest rates was wrong and today rates are even lower. The formerly unimaginable low rates of Japan (0.53%) are no longer the outlier in the developed world. Shockingly, Greece and Portugal, whose fiscal crises some considered to be threatening the euro itself, can now borrow like Japan in 2014. As we see from the chart, among all developed economies, the US has the highest rates now and in 2014. On one hand, relatively high rates in the US are puzzling, since from a pure risk and return perspective, the US is generally considered the most trustworthy market in the world. On the other hand, higher rates in the US could be an expectation of higher potential for growth. Clearly, these rates are determined by a complex market equilibrium involving far more than just the central banks; we still don’t know whether interest rates will rise.

Low rates and high valuations isn’t a phenomenon confined to government issued bonds. Corporate and high yield bonds spreads are also historically low and stock valuation ratios are relatively high. US rates may or may not go up. But the bottom line is that US Treasurys are not an inferior asset class. At New Frontier we do not forecast. We statistically evaluate current market conditions and use patented rebalancing and optimization that test and process thousands of scenarios. The result is portfolios exposed to global growth and durable by design to weather current and future risks. In this global and multi-asset context, US Treasurys are worth thoughtfully including in a portfolio.

Disclosures:

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The indices are not investable securities. Any investable security would have performance reduced by fees and expenses. Any distribution must comply with your firm’s guidelines and applicable rules and regulations, including Rule 206(4)-1 under the Investment Advisers Act of 1940.

comments powered by Disqus

Locate Us

New Frontier Advisors

155 Federal Street

Boston, MA 02110

617.482.1433

Contact us to find out how you can invest in New Frontier portfolios.