60/40: Alive and Well when Optimized

Once again skeptics are challenging the notion that the 60/40 portfolio still works. Some fundamental misunderstandings around what constitutes an optimized approach to comprehensive portfolio management continue to fuel the negative narrative.

With very low interest rates raising doubt about the fixed income component of 60/40, riskier alternatives are touted as a solution to higher returns. Meanwhile, equity markets are near all-time highs, triggering concerns about an equity bubble. New Frontier’s approach to modern asset management offers an optimal solution to address these issues.

The reality is that investors who have stayed in a portfolio of 60% U.S. stocks and 40% bonds have been rewarded. New Frontier’s 60/40 indices, which mirror our global and domestic balanced portfolios, reached all-time highs in 2021, and other indices show strong performance[1] over multiple time frames.

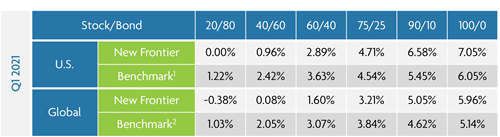

New Frontier Global & U.S. Index Q1 Performance

Data as of 03/31/2021.

1 U.S. Benchmark: Blended S&P 500 NR / 3 Month T-Bill 2 Global Benchmark: Blended MSCI ACWI IMI NR / 3 Month T-Bill

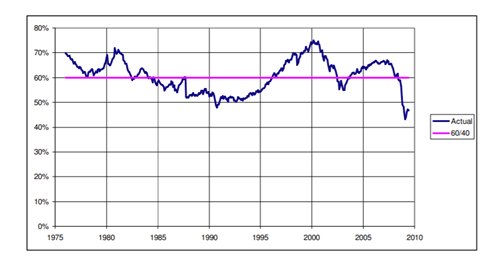

Furthermore, the balanced portfolio will always be fundamentally important for investors. On a conceptual level, all investable securities over time equate roughly to a 60/40 portfolio. In fact, Nobel Prize winner Bill Sharpe’s research shows that the sum of all investable assets in the world of stocks, bonds, and other securities closely resembles 60/40[2]; therefore, the portfolio held on average over time by most investors is essentially a 60/40 portfolio.

The Ratio of the Value of U.S. Stocks to U.S. Stocks plus Bonds, Jan. 1976 through June 2009

It is the middle of the road portfolio that ends up as most appropriate for what many investors are trying to achieve.

Sophisticated asset management addresses common concerns with multi-asset class portfolios. Here are the key components of New Frontier’s active approach to investing with passive ETFs:

- Optimized at the core. Optimization is about making the most informed, most efficient, and most intensive decision. That includes building a sophisticated portfolio with many different ETFs representing a variety of asset classes to eliminate any inefficiencies in the portfolio. This allows investors to get every bit of return possible from their portfolio and to avoid unrequired risk.

New Frontier’s portfolio is optimized over thousands of potential investment scenarios to maximize the performance at all times. That means doing quite a bit more than simply placing people in stylized balanced portfolio risk buckets.

While traditional optimization methods do not work well, often creating poorly constructed portfolios, New Frontier invented a unique patented technology that addresses the problems of current methods, resulting in far better risk-managed funds.

- Highly diversified across many factors. A well-constructed 60/40 portfolio has exposure to a wide range of securities and is called a balanced portfolio for a reason. Not only does it balance the risks of stocks and bonds, but when executed well, it also balances risks across all asset classes. Further, the balanced portfolio is simply the most flexible portfolio structure, allowing for maximum exposure across all asset classes.

A case in point, New Frontier’s portfolio consists of 27 ETFs across 26,000 securities spanning all liquid asset classes, risk factors, and regions. At the other end of the portfolio spectrum are 60/40 portfolios comprised of just one stock fund and one bond fund – this doesn’t meet a minimum threshold for proper portfolio construction.

- Adaptive approach at each point in time. A properly designed 60/40 portfolio is positioned to dynamically balance the risk and return tradeoff of duration, credit, and all equity sources of return to capture global economic growth across all asset classes. New Frontier continuously reevaluates capital market expectations using the latest available data, including full yield curve and credit spread values, to build a portfolio that has the most favorable exposures at each point in time.

A dynamic approach to building a balanced portfolio is crucial in light of market shifts. For example, China and tech stocks had very different characteristics post-pandemic than pre-pandemic. Some parts of the world are looking more like a value type of investment as their prices go down, and the interest rate environment is changing dramatically. Our portfolios adapt flexibly to account for these changes.

- Rebalancing via an objective test. Going with one’s gut or trying to speculate on the future is not advisable, to say the least, and an impossible exercise. That’s why an objective, statistically rigorous litmus test, like the Michaud-Esch Rebalancing Test as to when to rebalance portfolios is a crucial part of any well-defined asset management program.

Because the hypothetical optimal portfolio is always changing, rebalancing should not be done on a calendar or rigid rules-basis, but when the data says it’s warranted. In past years, we have rebalanced as infrequently as once a year but lately, we have rebalanced more than ever - four times in 2020 for our core strategies is a new record for us.

- Accommodates a low interest rate environment. In these times, some investors may eschew bonds fearing interest rates will rise. While bonds may generate little income in nominal terms, this misses the point of bonds in a comprehensively managed portfolio. Fixed income exposure manages risk and also helps balance worries about bursting of the asset bubble. When investors shift out of bonds in favor of alternatives, they are likely to lose on average while adding risk.

- Alternatives carefully considered. Not all alternatives belong in risk-targeted investment portfolios for most investors. Exposure to alternatives with unique properties or positive risk premia such as commodities and real estate to enhance the risk-adjusted return of the 60/40 portfolio can be appropriate. However, derivatives, speculative assets, or side bets do not belong in the balanced portfolio, as they do not typically reward investors relative to their risk.

- Built for the long-term. It’s important to focus on mitigating risk in the balanced portfolio over long time horizons. Not betting on any one asset class and investing in global economic growth opportunities as the most reliable source of return helps ensure portfolio longevity.

It’s also helpful to note that compound return is not average return. Portfolio compound return is key to designing investment strategies that optimally meet long-term objectives. All New Frontier portfolios are optimal compound return investments.

As capital is infused into the markets in the context of the current interest rate environment, achieving returns may look different than in the past. However, modern portfolio strategy should not include tossing out 60/40, but instead an infusion of new innovations like the multi-patented ones upon which our firm was founded. Through an optimized approach, we are redefining what sophisticated asset management looks like and how returns are achieved, for the benefit of investors at large.

Disclosure:

Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. The indices are not investable securities. Any investable security would have performance reduced by fees and expenses. Any distribution must comply with your firm’s guidelines and applicable rules and regulations, including Rule 206(4)-1 under the Investment Advisers Act of 1940.

_________________

[1] MSCI World index (60) and Bloomberg Barclays U.S. Aggregate (40) show a five-year annualized return of 10.2%,

[2]Sharpe, William F., Adaptive Asset Allocation Policies (May 25, 2010). Financial Analysts Journal, Vol. 66, No. 3, 2010

comments powered by Disqus

Locate Us

New Frontier Advisors

155 Federal Street

Boston, MA 02110

617.482.1433

Contact us to find out how you can invest in New Frontier portfolios.