15 Years of ETF Investing: What Have We Learned?

A market milestone was reached this past August when assets invested in index-based mutual funds and ETFs surpassed the amount invested in active equities for the first time. Passive investment strategies have been growing for decades at the expense of actively managed funds. Of course, index-based mutual funds have been around since the 1970s, yet the explosive rise of passive investing would not have been possible without the extraordinary growth of ETFs over the past 15 years.

ETFs themselves owe much of their growth to the success of portfolios and investment strategies based on ETFs. Barely a blip on the radar screen when New Frontier began to use ETFs to build optimized investment strategies, today they are widely used by all types of investors, from individuals to sophisticated asset managers and hedge funds managing billions. As one of the very few early ETF strategists still active, New Frontier is ideally placed to look back at the evolution of ETF investing and reflect upon the remarkable trajectory of one of the most important financial engineering products in modern finance.

The Early Days of ETF Investing

Sophisticated ETF portfolio strategies first arrived in 2004 due to a convergence of factors. The burst of the Dot-com bubble created greater demand for professionally-managed accounts among retail investors. Asset managers and wealth advisors evolved from picking individual stocks and mutual funds to focusing on the importance of well-defined, globally diversified multi-asset investment strategies. At the same time, new technology platforms were emerging to support financial advisors and their clients, enabling retail investors to access institutional quality strategies for the first time.

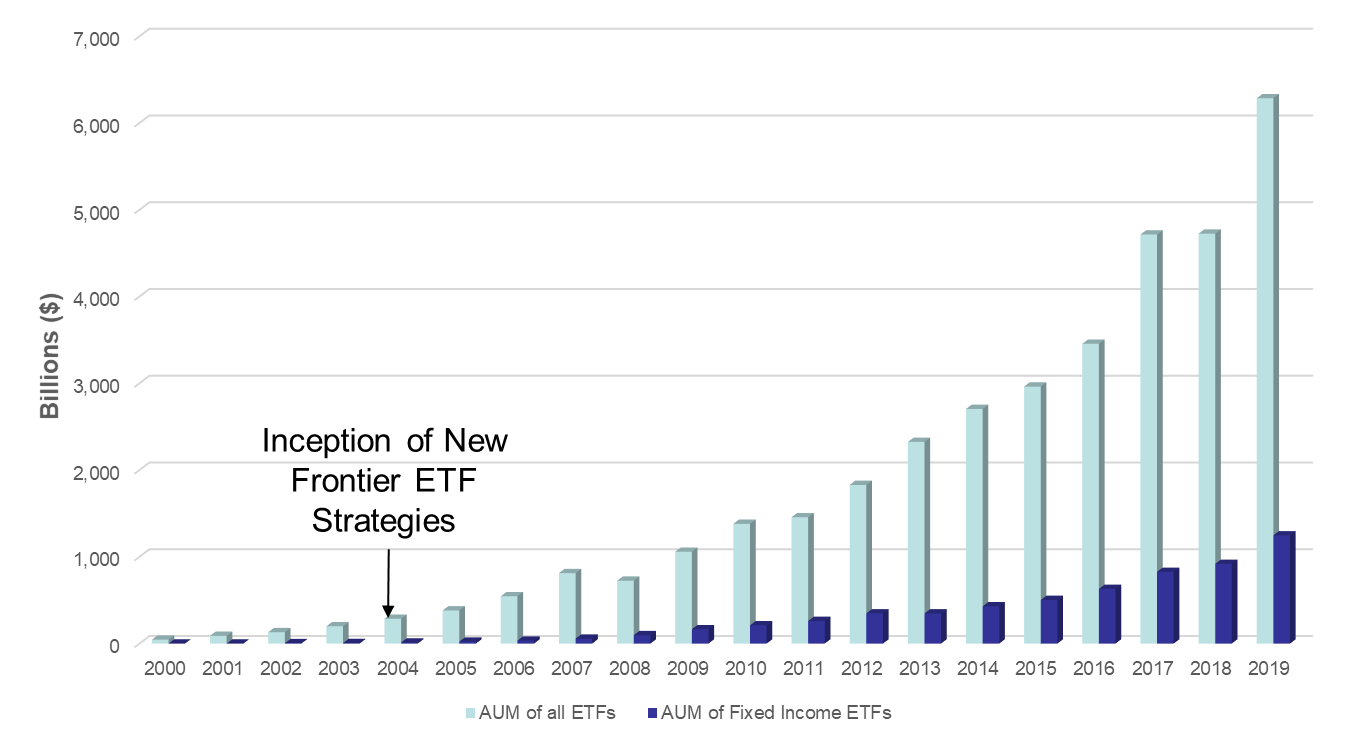

In 2004, ETF management was in its infancy. There were only a few mature equity ETFs and even fewer tradable fixed income ETFs available. By the end of 2004, it became possible to invest in a limited number of institutional quality global and domestic stock and bond index ETFs. As Figure 1 below indicates, the market for ETFs grew rapidly from those protean times. In October 2004, we launched the New Frontier Global ETF core portfolios for six systematic stock/bond risk levels from 20/80 to 100% equity indices. We applied our multi-patented optimization and investment management technology to develop institutional quality core asset allocation strategies entirely on low-risk, low cost, tax efficient index ETFs. New Frontier became perhaps the first manager to construct global, multi-asset, institutional quality portfolios out of index ETFs.

Early skeptics had misgivings of the viability of fixed income index ETFs in particular and, more generally, whether ETFs were structurally inferior to mutual funds. However, fixed income ETFs became more popular over the next four years, and received a further boost from the global financial crisis in 2008 as investors fled equities in search of safe havens. Fixed income ETFs proved reliable, and their returns benefited from Fed policy designed to drive down interest rates. The doubters dissipated over time.

Figure 1

The ETF Landscape Evolves

The growth rate of Exchange Traded Products increased dramatically after 2004 as ETF-based portfolios became more prevalent.

Over the next decade, innovations continued in the ETF space as investable assets such as gold and real estate became more tradable, individual country funds enabled more precise global investing, and funds with targeted exposures, such as low volatility, allowed for better risk management. With the explosion of choices, however, it has become harder to evaluate the long-term viability among many. Careful quality control analysis is very much an important factor for developing and maintaining an institutional grade global multi-asset ETF portfolio.

Better Analysis, Lower Costs

Over the years, ETF liquidity has also improved dramatically. Capital market prices are often so reliant on ETFs that price discovery may occur in the ETF market rather than in stock or fixed income markets. This past Veterans Day saw spreads of a penny between bid and ask prices in large volumes on most bond ETFs even though the bond markets were closed. ETF prices are often the best way to assess what is going on in international markets while markets are closed.

ETF portfolios also benefit from advancements in technology. Whereas in early days portfolio trades could take weeks to implement, today even sizable trades take only minutes, if not seconds. And while ETFs were always more tax efficient than mutual funds, ETF issuers have improved efficiency to the point where major providers announced that 100% of their ETFs had zero capital gains in 2019.

As ETF portfolios gained prominence and liquidity, new analytical tools have emerged. Measuring liquidity and quantifying risk pre-trade was once a massive challenge. Today, trading platforms, with their decades of back data, have made this process routine. For 2020’s institutional investors, it is now a simple matter to quickly move tens or even hundreds of millions of dollars from one ETF to another, with accurate ways to model those transactions in advance.

Meanwhile, the total cost of ownership—always a major selling point for ETFs—continues to fall. According to Morningstar, the asset-weighted ETF expense ratio has fallen by half over the past decade,[1] and the industry is rapidly careening towards a nominal zero-fee environment. Since 2004, retail commissions have gone from $59.95 per trade to free in many cases in late 2019. The present “free trade war” has enormous implications for ETF trading platforms, enabling more ETFs in smaller accounts with more frequent trading.

Portfolios of ETFs Today: Endless Possibilities

New Frontier has long claimed that index ETFs are the security of choice to implement an institutional grade long-term reliable investment process for investors. The stability and robustness of ETFs provide nearly endless possibilities for well-defined index ETF based strategies. They are a natural framework for proving how state-of-the-art risk management technologies can deliver enhanced risk-adjusted returns to clients.

New Frontier ETF strategies have evolved with increasing sophistication of available ETFs and acceptance by investors. In 2004, our core stock/bond multi-asset strategies included only 12 index ETFs – nearly every institutional grade available. Today our strategies number nearly 30 ETFs covering a wide range of global and domestic equity, fixed income, real estate, and commodity indices. Our multi-patented optimization and portfolio management technologies have facilitated efficient risk management of a wide variety of new ETFs including international bonds, small cap stocks, real estate funds, corporate and emerging market debt, country-specific products, bank loans, and short high-yield products. Our research has kept pace with the need to manage larger and more varied ETF investment strategies. Our portfolio rebalancing need-to-trade technology now allows daily portfolio risk monitoring and various efficiencies have improved our ability to better optimize and recommend more efficient trades.

Today the future of ETF investing looks bright as new developments continue to benefit investors. The value proposition continues to resonate with retail and institutional investors alike, and we expect the market will continue to thrive in coming years, so long as their foundational achievements to date—enabling deeper liquidity, transparency in both pricing and performance, and investing in innovation—remain at the core of the ETF market.

[1] https://newsroom.morningstar.com/newsroom/news-archive/press-release-details/2019/Morningstars-Annual-Fee-Study-Finds-That-in-2018-Investors-Paid-Less-to-Own-Funds-Than-Ever-Before/default.aspx

comments powered by Disqus

Locate Us

New Frontier Advisors

155 Federal Street

Boston, MA 02110

617.482.1433

Contact us to find out how you can invest in New Frontier portfolios.